{kind=link}

The dangerous information: Virtually half are usually not ready.

In a latest examine, we used our up to date Nationwide Retirement Danger Index (NRRI) to see whether or not households have a great sense of their very own retirement preparedness – do their expectations match the fact they face? That’s, do households in danger know they’re in danger? Understanding households’ self-assessed retirement preparedness is essential as a result of households that aren’t frightened sufficient won’t save sufficient and households which might be too frightened will unnecessarily sacrifice their pre-retirement lifestyle.

The Survey of Client Funds (SCF), which is used to assemble the NRRI, asks every family to price the adequacy of its anticipated retirement earnings. The query’s response scale is from one to 5, with one being “completely insufficient,” three being “sufficient to take care of dwelling requirements,” and 5 being “very passable.” Thus, any family that solutions one or two considers itself to be in danger.

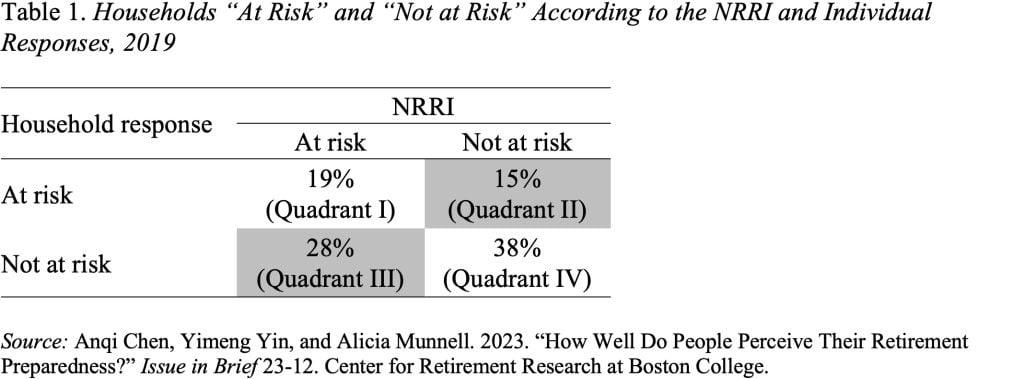

We in contrast every family’s self-assessed danger with the family’s estimated danger from the NRRI. The outcomes present that for 57 p.c of households their self-assessment agrees with the NRRI (Quadrants I and IV in Desk 1); 43 p.c of households get it mistaken (see the shaded parts). Fifteen p.c (Quadrant II) are “too frightened” – they report being inadequately ready however the NRRI says that they don’t seem to be in danger. Twenty-eight p.c (Quadrant III) are “not frightened sufficient.”

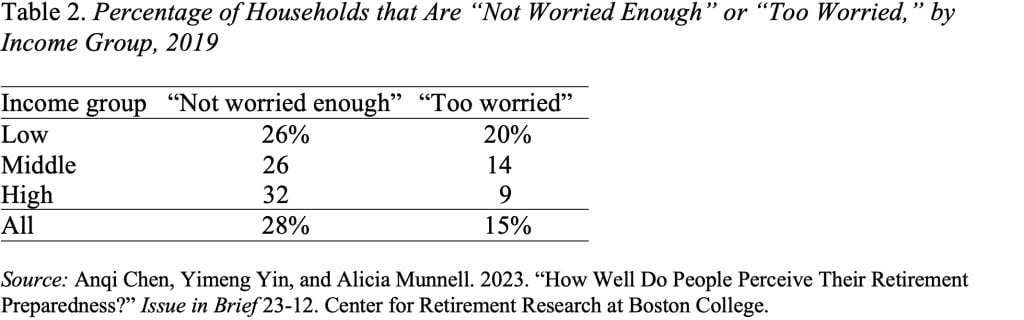

The query is why do households get it mistaken? Outcomes by earnings present that high-income households – maybe overreacting to the affect of the sturdy financial system on housing and inventory costs throughout the 2013-2019 interval – are the more than likely to be “not frightened sufficient” and low-income households are the more than likely to be “too frightened” (see Desk 2).

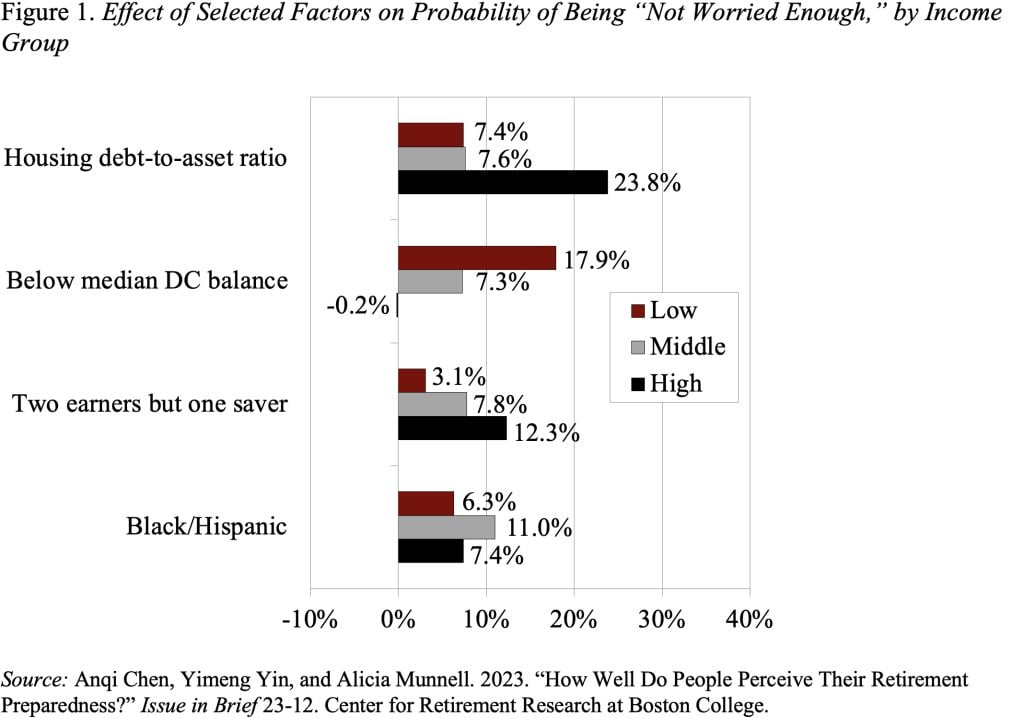

The evaluation used regressions for every earnings group to elucidate the connection between numerous components and the likelihood of households ending up being “not frightened sufficient’ or “too frightened.” Households that had been overly optimistic in regards to the financial restoration or overestimated how a lot earnings their belongings may present had been extra more likely to be “not frightened sufficient.” Their overconfidence might make them underestimate potential dangers. Subsequently, it’s not stunning that households with greater housing debt-to-asset ratios, comparatively low asset balances in 401(ok)s and different outlined contribution (DC) plans, and two earners however just one saver had been extra more likely to be “not frightened sufficient” (see Determine 1).

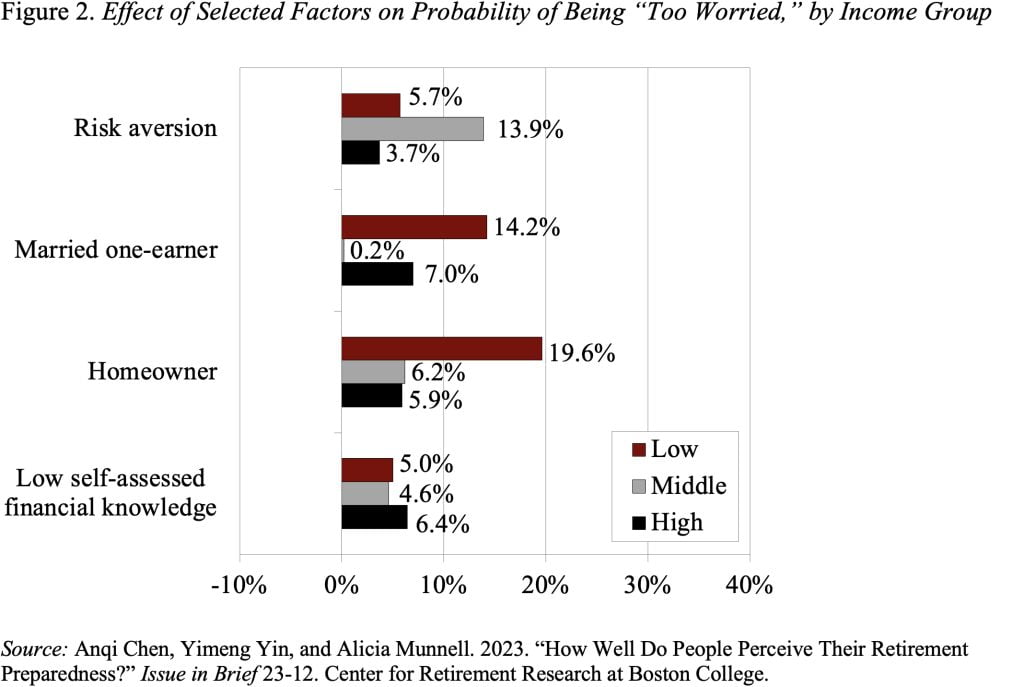

In contrast to overly optimistic households, those that are “too frightened” are usually not conscious of how a lot earnings they’ll have in retirement and maybe have much less optimism within the asset markets. Traits that seize these components – reminiscent of danger aversion, married one-earner households, home-owner, and low self-assessed monetary information – predicted households’ probability of being “too frightened” (see Determine 2).

The underside line is that 47 p.c of immediately’s working households are in danger – 19 p.c understand it and 28 p.c don’t. Each teams need assistance.

The important thing message, nonetheless, is almost three-fifths of households have a great intestine sense of their monetary state of affairs and, within the combination, households’ self-assessments intently mirror the outcomes produced by the NRRI. These findings counsel that insufficient retirement preparedness is certainly a widespread drawback.