{kind=link}

Kim Moody: Canada must take a tough have a look at decreasing private tax charges and guarantee individuals hold a minimum of half of all good points

Critiques and suggestions are unbiased and merchandise are independently chosen. Postmedia could earn an affiliate fee from purchases made by way of hyperlinks on this web page.

Article content material

Earlier than 2015, Alberta had, by far, the bottom federal-provincial mixed high marginal tax fee in Canada at 39 per cent. This comparative benefit contributed enormously to massive quantities of funding and folks going into Alberta.

That 12 months, nonetheless, the federal Liberal Occasion shaped the brand new authorities, and in Alberta, the NDP surprisingly got here to energy provincially. The brand new federal authorities promptly introduced it was elevating the charges on so-called high-income earners by “asking them to pay just a bit bit extra” (an offensive talking level that was overused for the subsequent four-plus years, particularly when one understands how a lot high-income earners already pay when in comparison with the entire of Canada). The brand new “ask” would start in 2016 by introducing a brand new excessive federal bracket that elevated the top-end fee by 4 per cent.

Commercial 2

Article content material

Article content material

The Alberta authorities additionally launched new greater charges for 2015 and 2016. When the mud settled, Alberta’s highest marginal private tax fee elevated to a high finish of 48 per cent, a big improve from its earlier low and considerably narrowing the hole between among the provinces that already had excessive private charges, reminiscent of Ontario, Quebec and among the Maritime provinces.

After the 4 per cent federal improve, Ontario, Quebec and the Maritime provinces had private charges of greater than 50 per cent. Ontario settled right into a mixed federal–provincial tax fee of 53.53 per cent and it stays that as we speak. Quebec and the Maritime provinces are comparable. British Columbia not too long ago joined that membership.

Bluntly, Canada’s marginal private earnings tax charges are far too excessive. After I point out this to a few of my left-leaning mates, they could rebut: “Kim, you notice that Canada’s highest marginal charges traditionally have been within the 80-plus-per-cent vary … proper? From that comparability, our present highest charges are a cut price.”

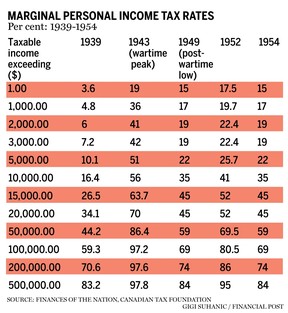

Technically, they don’t seem to be mistaken. Take a look on the knowledge within the accompanying desk from a 1954 publication, Funds of the Nation, by the Canadian Tax Basis. You’ll rapidly see that the very best marginal charges topped 80 per cent, with the excessive being 97.8 per cent in 1943.

High Tales

Article content material

Commercial 3

Article content material

However let’s put a few of that into context. First, Canada’s private earnings tax system was comparatively younger from the Nineteen Thirties to the Fifties. The quantity of precise taxpaying people in comparison with the inhabitants as a complete was very low in comparison with as we speak. As well as, capital good points weren’t taxable again then (capital good points didn’t develop into taxable in Canada till 1972). So, in fact, there was no scarcity of gamesmanship taken by the small variety of high-income taxpayers to transform their earnings into non-taxable capital good points.

In 1962, the federal authorities — led by John Diefenbaker — had the braveness to convene The Royal Fee on Taxation to assessment the complete taxation system and make suggestions about what Canada ought to do. In 1966, the Royal Fee launched its voluminous report and suggestions. Relating to private tax charges, the report acknowledged this in Chapter 11:

“We’re persuaded that top marginal charges of tax have an adversarial impact on the choice to work relatively than take pleasure in leisure, on the choice to save lots of relatively than devour, and on the choice to carry property that present financial returns relatively than property that present advantages in variety. We predict there could be nice benefit in adopting a high marginal fee no larger than 50 per cent. With such a most marginal fee, taxpayers could be assured that a minimum of half of all good points could be theirs after taxes. We predict there’s a psychological barrier to larger effort, saving and worthwhile funding when the state can take a couple of half of the potential acquire.”

Commercial 4

Article content material

In 1974, American economist Arthur Laffer mentioned the same subject when he mused in regards to the relationship between taxation charges and the ensuing ranges of presidency tax income. The “Laffer curve” assumes that no tax income is raised on the excessive tax charges of zero per cent and 100 per cent, which means that someplace between these extremes is a fee that maximizes authorities tax income. Discovering that most fee is a difficult train for governments.

In my expertise, private behaviours considerably change when private tax charges method 50 per cent (much like what the Royal Fee mentioned in its report above). Folks will seek for methods to decrease their tax payments, particularly when the notion is that there’s not a lot worth being offered when in comparison with the fee (or, as many politicians say, “funding”).

There’s a purpose why important quantities of high-income earners/rich individuals have not too long ago been leaving Canada. And it’s the identical purpose why this nation has a troublesome time attracting top-end expertise in drugs, biotech, expertise, skilled sports activities and different industries/professions. Each time I increase this alarm bell, I routinely get a rebuttal that I’m exaggerating. I’m not.

Commercial 5

Article content material

Associated Tales

-

New tax guidelines may imply donating extra to charity this 12 months

-

Rejection of CRA expense denial candy music to taxpayer’s ears

-

Tax system not constructed to maintain up with inflation

Canada must take a tough have a look at this difficulty to decrease private tax charges and guarantee folks that “a minimum of half of all good points could be theirs.” And it’d go a good distance to enhance its lagging productiveness … an vital subject for one more day.

Kim Moody, FCPA, FCA, TEP, is the founding father of Moodys Tax/Moodys Personal Shopper, a former chair of the Canadian Tax Basis, former chair of the Society of Property Practitioners (Canada) and has held many different management positions within the Canadian tax neighborhood. He could be reached at kgcm@kimgcmoody.com and his LinkedIn profile is www.linkedin.com/in/kimmoody.

Article content material

Feedback

Postmedia is dedicated to sustaining a energetic however civil discussion board for dialogue and encourage all readers to share their views on our articles. Feedback could take as much as an hour for moderation earlier than showing on the location. We ask you to maintain your feedback related and respectful. We’ve enabled e mail notifications—you’ll now obtain an e mail in case you obtain a reply to your remark, there’s an replace to a remark thread you comply with or if a consumer you comply with feedback. Go to our Group Tips for extra data and particulars on easy methods to regulate your e mail settings.