{kind=link}

For those who don’t imagine mortgage charges and residential costs can fall collectively, simply take a look at what house costs have finished within the face of seven% mortgage charges.

Regardless of the 30-year mounted surging from sub-3% ranges to near-8% ranges in lower than two years, house costs hit contemporary all-time highs.

So why is it so tough to think about the alternative situation, the place each rates of interest and property values fall in tandem?

It appears the human thoughts desires there to be an inverse relationship between charges and costs when there typically isn’t.

The excellent news is it’s potential that each charges and costs average from right here, ushering in a greater degree of housing affordability.

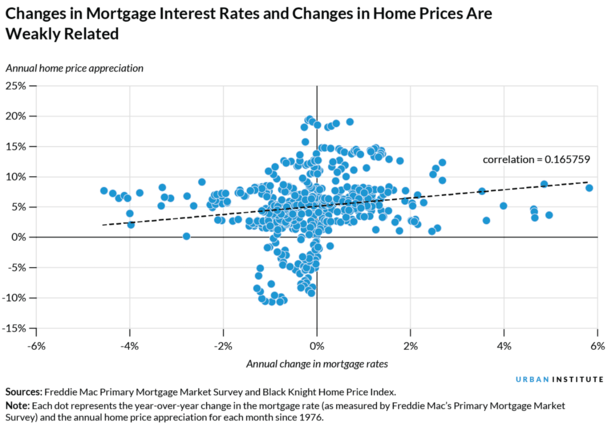

Dwelling Costs and Mortgage Charges Don’t Have A lot of a Relationship

The City Institute wrote an article final yr in regards to the relationship between house costs and rates of interest when mortgage charges have been quickly ascending.

They famous that since 1976, there was “a optimistic however weak relationship” between the 2.

In different phrases, greater mortgage charges are sometimes accompanied by greater house value appreciation, although this tendency isn’t sturdy.

Nonetheless, it defies the logic many housing bears and on a regular basis people possess, the place they assume greater mortgage charges should equate to decrease house costs.

In any case, if it turns into costlier to buy a house, the value should come down. That’s their argument no less than.

However while you take a look at different needed gadgets (shelter additionally being a necessity), individuals don’t cease shopping for them as a result of the fee goes up.

And one additionally wants to contemplate why mortgage rates of interest are excessive to start with. Usually, rates of interest are excessive as a result of the financial system is working scorching.

This implies there are extra shoppers on the market making extra money, which ostensibly means extra of them can afford to purchase costly homes.

One different issue to contemplate is all-cash patrons – a big share of house patrons forgo mortgages to get the deal finished, particularly buyers.

So whereas greater rates of interest would possibly have an effect on the typical house purchaser, they don’t have an effect on everybody.

Dwelling Costs and Inflation Have a Sturdy Constructive Relationship

Whereas greater mortgage charges and residential value appreciation have a weak, however nonetheless optimistic relationship, inflation and residential value appreciation have a robust one.

That’s to say {that a} greater fee of inflation is related to greater house value appreciation.

And this affiliation is considerably stronger than the connection between mortgage charges and residential costs.

Inflation has been entrance and middle for the previous couple years, and the Fed has been actively combating it by way of 11 fed funds fee hikes since early 2022.

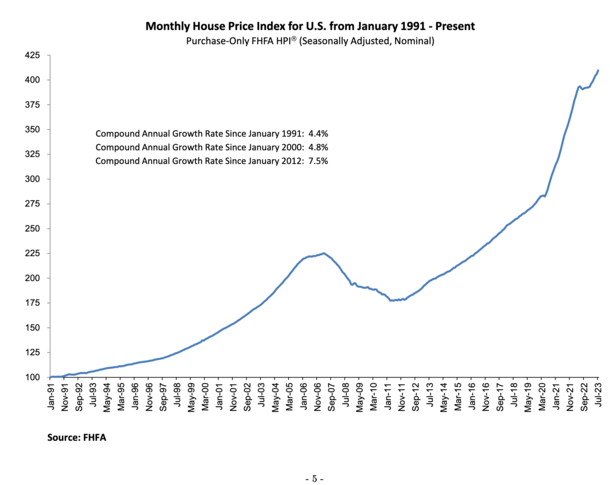

On the identical time, house costs haven’t fallen, although the speed of appreciation has. Nonetheless, when you think about the 30-year mounted greater than doubling in such a short while span, you’d anticipate housing market carnage.

As an alternative, we’ve seen house costs hit new all-time highs. Final week, the FHFA reported that house costs have been up 0.8% in July from a month earlier, and up 4.6% year-over-year.

Whereas which may sound too good to be true, think about that prime rates of interest are sometimes correlated with durations of sturdy financial development, low unemployment, rising wages, and excessive inflation.

Put one other method, when the financial system is scorching, house costs are inclined to rise as a result of extra individuals have cash and jobs to assist mortgage funds, even when they develop bigger.

This implies housing demand can improve or no less than stay regular, even when affordability erodes over time.

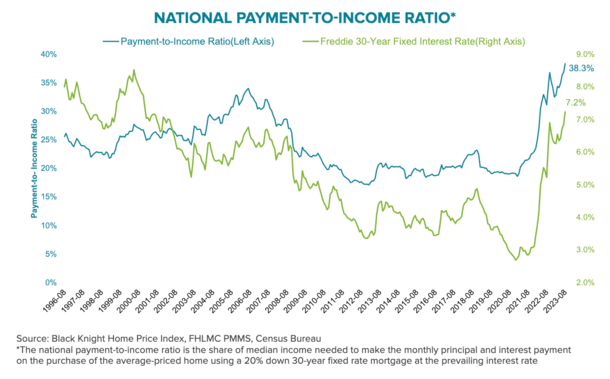

Housing Affordability at Its Worst Since 1984

After all, affordability has worsened considerably of late as a result of each charges and costs have continued to rise, pushing the nationwide payment-to-income ratio to its highest degree since 1984.

Per Black Knight, it takes a $2,423 principal and curiosity fee to buy the median-priced house with 20% down and a 30-year mounted mortgage.

That is up 91% from $1,155 simply two years in the past, when the Fed ended Quantitative Easing (QE) and commenced their marketing campaign often known as Quantitative Tightening (QT).

Clearly this has slowed house value appreciation, which had been working at a double-digit clip. However as famous, costs carry on rising.

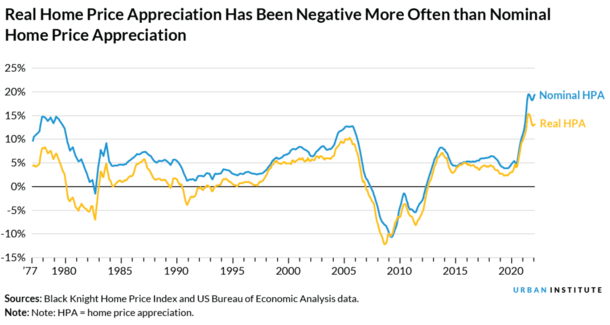

Nominal Dwelling Costs Are Sticky and Hardly ever Fall

The City Institute famous that mortgage charges have principally simply declined since 1976.

There have solely been just a few durations when charges elevated greater than 1.5 share factors year-over-year.

Nonetheless, charges did rise quickly from September 1979 to March 1982 (bear in mind these Nineteen Eighties mortgage charges) and from September 1994 to February 1995.

This prompted the speed of house value appreciation to gradual rapidly, much like what we noticed currently.

Throughout that 1979 to 1982 mortgage fee rise, house value appreciation decelerated from 12.9% to simply 1.1%.

And from September 1994 to February 1995, it slowed from 3.2% to 2.6%.

Throughout every of those time durations, actual house value appreciation (adjusted for inflation) went detrimental, however nominal house costs solely went detrimental as soon as a recession was beneath method.

In different phrases, you want the financial system to collapse if you’d like house costs to return down. And guess what may additionally come down on the identical time?

What About Falling Dwelling Costs Mixed with Decrease Mortgage Charges?

So we’ve mentioned how house costs and mortgage charges can rise collectively, although the connection isn’t a robust one.

However {that a} sturdy financial system tends to raise house costs greater, as has been the case over the previous a few years.

If that’s true, can’t the alternative even be appropriate? Can’t mortgage charges and residential costs fall on the identical time, maybe due to disinflation and a cooling financial system?

The reply is sure they will. If and when the financial system takes a flip for the more severe, the Fed may pivot and start slicing its personal coverage fee.

On the identical time, mortgage charges may retreat from current highs and make their method decrease as properly.

And residential costs may additionally start to fall as a recession units in, leading to job losses, pay cuts, greater unemployment, and decrease housing demand.

This counters the notion that mortgage charges again within the 4-5% would set off one other housing market frenzy crammed with bidding wars and quickly appreciating costs.

Merely put, if house costs and mortgage charges can rise collectively, they will additionally fall collectively.

Ideally, we see moderation on each fronts, with house costs perhaps pulling again from current highs, no less than on an actual, inflation-adjusted foundation, whereas mortgage charges additionally ease.

This might assist to deal with the affordability points at the moment plaguing the housing market.

Simply bear in mind although that the opposite large drawback is provide. There merely aren’t sufficient houses on the market, and as everyone knows, shortage results in greater costs.