{kind=link}

The child boomers born within the early Sixties, on the tail finish of the demographic wave, had about $280,000 in retirement wealth once they reached their early 50s. That’s considerably much less – about $50,000 much less – than the late-Nineteen Fifties boomers had on the identical age.

A few of this shortfall may’ve been anticipated for the youngest boomers. Every new crop of boomers has taken a much bigger hit of their Social Safety checks as a result of the statutory age for accumulating the complete month-to-month profit has been creeping up. The shrinking checks are in opposition to the backdrop of dwindling pensions. (Retirement wealth consists of the present worth of employee’s future Social Safety and conventional pension advantages, in addition to retirement financial savings.)

However, whereas Social Safety and conventional pensions are smaller, the decline in late boomers’ wealth general was not preordained. They had been the primary era to have entry to a 401(ok)-style retirement plan for his or her whole careers, and so they might’ve accrued sufficient cash in financial savings to make up for the opposite losses. However they didn’t.

The one largest motive for the shortfall in financial savings was the ten % spike in unemployment in the course of the Nice Recession that adopted the inventory market crash, finds a brand new research that separates out the financial and demographic causes behind the decline in late boomer households’ wealth.

The unemployed had been pressured to cut back contributions to employer retirement accounts, and the monetary injury was worse for the late boomers than for the individuals born earlier within the child increase. The “hyperlink between work and wealth accumulation declined considerably for late boomers, in comparison with mid-boomers,” the researchers defined.

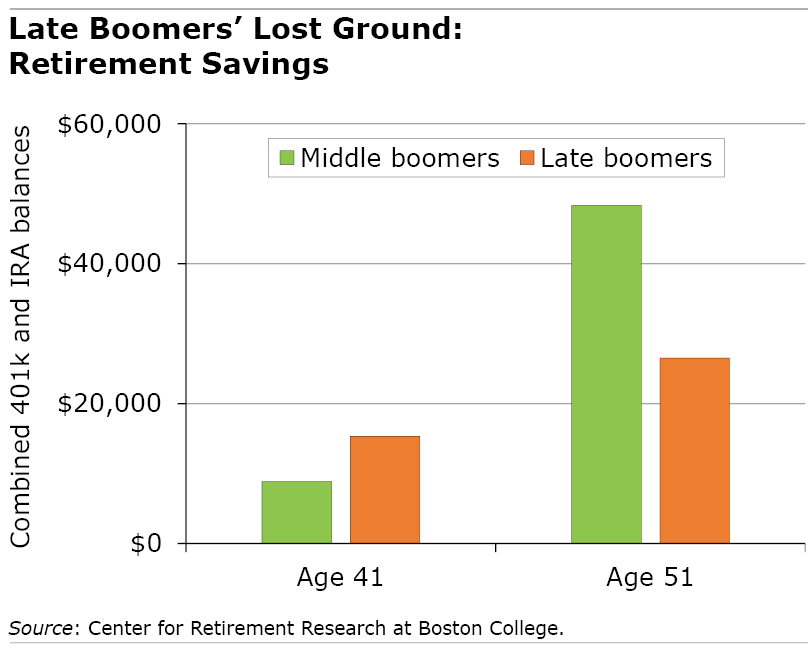

Previous to the Nice Recession, the late boomers had been forward of the employees who had been born earlier within the increase. At age 41, late boomers had $15,329, on common, of their 401(ok)s and IRAs – considerably greater than the center boomers born within the late Nineteen Fifties had saved by that age.

However after the recession, the tables had turned. By age 50, late boomers had round $28,000 in financial savings – half of what the mid-boomers had at 50.

The weak labor market took its toll in two methods. The late boomers’ employment charge, which had been 98 % earlier than the Nice Recession, dropped beneath 80 % a decade later and stayed there for a number of years. These newly unemployed staff misplaced the flexibility to avoid wasting in a 401(ok) or might even have been pressured to withdraw cash to pay payments.

The recession didn’t spare the late boomers who remained employed both, and their 401(ok)s took an oblique hit. Earnings tends to stage out or decline round age 50, however the late boomers’ incomes fell sharply of their 40s, that are often the height incomes years. At 50, their family earnings averaged round $73,000, in contrast with $104,000 and $88,000, respectively, for early and mid-boomers at 50.

Smaller paychecks translate to smaller 401(ok)s, as a result of some individuals cease contributing altogether. If staff do sustain their common 401(ok) contributions, the quantities are smaller as a result of contributions are a set proportion of a employee’s earnings.

Demographic modifications have additionally decreased late boomers’ common wealth accumulation however to a lesser extent. Folks of colour have vastly much less wealth than Whites, and the Hispanic and Black populations have grown, in order the retired inhabitants turns into extra various, common balances look smaller.

Nevertheless, the wealth hole between staff of colour and White staff truly narrowed, principally as a result of their Social Safety wealth elevated.

The primary wrongdoer in late boomers’ misfortune was the Nice Recession – and which may be excellent news for the generations that observe. Because the financial calamity recedes within the rear-view mirror, “a number of the downward stress on wealth holdings ought to abate,” the researchers predicted.

To learn this temporary by Anqi Chen, Alicia Munnell, and Laura Quinby, see “What Occurred to Late Boomers’ Retirement Wealth?”

The analysis reported herein was derived in complete or partly from analysis actions carried out pursuant to a grant from the U.S. Social Safety Administration (SSA) funded as a part of the Retirement and Incapacity Analysis Consortium. The opinions and conclusions expressed are solely these of the authors and don’t signify the opinions or coverage of SSA, any company of the federal authorities, or Boston School. Neither america Authorities nor any company thereof, nor any of their workers, make any guarantee, categorical or implied, or assumes any authorized legal responsibility or accountability for the accuracy, completeness, or usefulness of the contents of this report. Reference herein to any particular industrial product, course of or service by commerce identify, trademark, producer, or in any other case doesn’t essentially represent or suggest endorsement, suggestion or favoring by america Authorities or any company thereof.