{kind=link}

However not all “high-risk” debtors are alike, so we want quite a lot of responses.

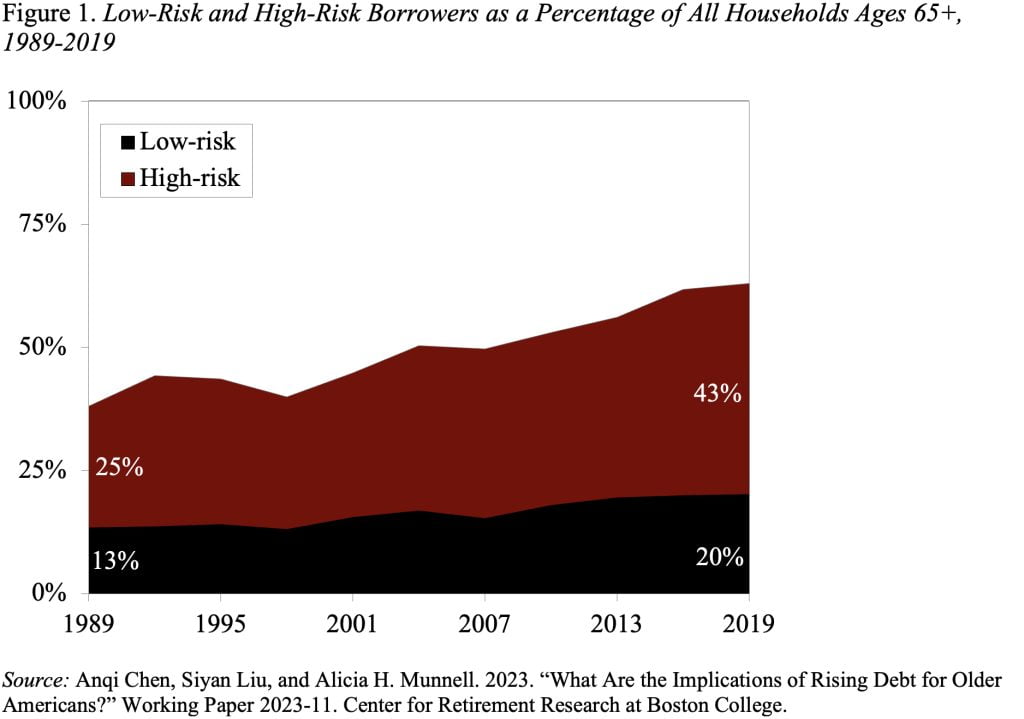

Policymakers and researchers have been fretting that the share of older Individuals with debt has risen from 38 p.c to 63 p.c since 1990. Having debt, nevertheless, doesn’t need to be a nasty factor. For instance, households that take out a low-interest mortgage to purchase a house, which generally appreciates, are probably making a savvy selection. In distinction, households that carry unpaid bank card balances may see their debt snowball, resulting in monetary misery. In a current research, my colleagues and I attempted to type out what share of households with debt had been at “excessive threat” and “low threat” of economic hardship and whether or not these at excessive threat typically appeared the identical or fell into distinct teams.

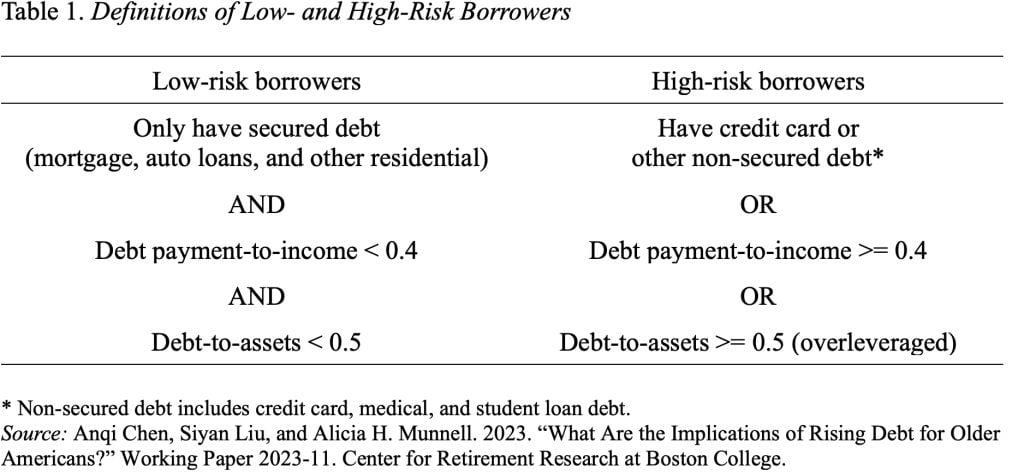

Step one was figuring out what number of of those households had been at excessive threat. The components – secured vs. unsecured debt, debt payment-to-income ratio, and debt-to-assets ratio – are generally utilized by lenders and different researchers (see Desk 1). Households with any revolving bank card debt are categorised as “excessive threat” since many of those debtors may expertise dangerous outcomes, regardless that the opposite debt measures wouldn’t seize them.

The outcomes of the classification train present that total progress is pushed by high-risk households (see Determine 1).

In occupied with coverage options, it’s important to determine how these high-risk households bought in bother. To do this, we used a method that exposed 4 clear subgroups of high-risk debtors.

- The most important group (33%) consists of “financially constrained” households, which have low ranges of wealth, are sometimes overleveraged, and wrestle with the necessities. This group is borrowing simply to get by.

- The second subgroup (26%) consists of “bank card debtors,” which incorporates middle-wealth households with no obvious have to borrow.

- The third subgroup (19%) is low/middle-wealth households whose housing debt funds devour over 40 p.c of their revenue. This group can be disproportionately non-White.

- The final group (23%) is “rich spenders.” Regardless of being within the high third of the wealth distribution, a couple of quarter of their revenue goes to debt funds, about 80 p.c have bank card debt, and over a 3rd have second properties.

What might be carried out to cut back the monetary vulnerability of high-risk debtors? Given their various traits, no one-size-fits-all resolution exists.

- Debt counseling and consolidation could assist the “financially constrained” households, however many wrestle to fulfill fundamental wants, in order that they want extra sources.

- “Bank card debtors” may gain advantage from conventional monetary counseling and laws requiring bank card issuers to supply higher info to customers.

- Households with “an excessive amount of home” would greatest be served by packages that cut back their housing burden, resembling refinancing or downsizing.

- Lastly, since many “rich spenders” have a second dwelling, promoting it’s one option to handle their debt.

The important thing takeaways from this research are: 1) the rising debt amongst older households shouldn’t be a benign phenomenon; and a pair of) the varied traits of high-risk debtors require quite a lot of coverage responses.