{kind=link}

Paying all money for a home is among the greatest methods to beat out your competitors and get a greater deal.

With all money, you do not have to submit a proposal with a financing contingency, which sellers dislike. Because of this, you enhance your possibilities of profitable a bidding conflict at an affordable value. Additional, with all money, you may be capable of get a bigger low cost.

I paid all money for a house in 2019 and was in a position to save about $100,000 – $150,000 off the market buy value. Being a neighbor, going twin company, writing a strong love letter, and having a quick shut had been additionally necessary variables.

Though paying all money makes the home-buying course of simpler, there are nonetheless some downsides to concentrate on. Let’s talk about!

The Downsides Of Paying All Money For A Home

The older I’ve gotten and the upper rates of interest go, the much less motivated I’m to tackle a mortgage to purchase a home.

Getting pre-approved for a mortgage is a cumbersome course of that requires numerous paperwork and an incredible quantity of persistence. There may be additionally the mortgage software price, which might simply run between $2,000 – $10,000. Therefore, if I can pay all money for a home, it’s my choice.

Nonetheless, there are downsides to every thing. These are the primary ones in case you’re contemplating paying all money for a house.

1) Capital positive factors tax

One technique to pay all money for a house is to lift funds by promoting different investments. The longer you personal your investments, often, the higher the positive factors. The secret is to attempt to promote your investments in a means that matches sufficient losers with winners to attenuate your capital positive factors tax.

However after a protracted bull market, paying capital positive factors taxes on asset gross sales may be an inevitability. Chances are you’ll finally be overwhelmed with too many winners.

The one technique to keep away from capital positive factors tax is in case you can make the most of uninvested money to purchase a house. You may even cut back your tax legal responsibility since you’ll now not must pay federal and state revenue taxes on the revenue earned by your money.

However except you by no means plan to promote your investments, you’ll finally must pay capital positive factors tax. It is good to promote shares every so often whenever you’ve earned sufficient to purchase no matter you need. In any other case, what is the level of investing within the first place?

2) You may miss out on additional positive factors

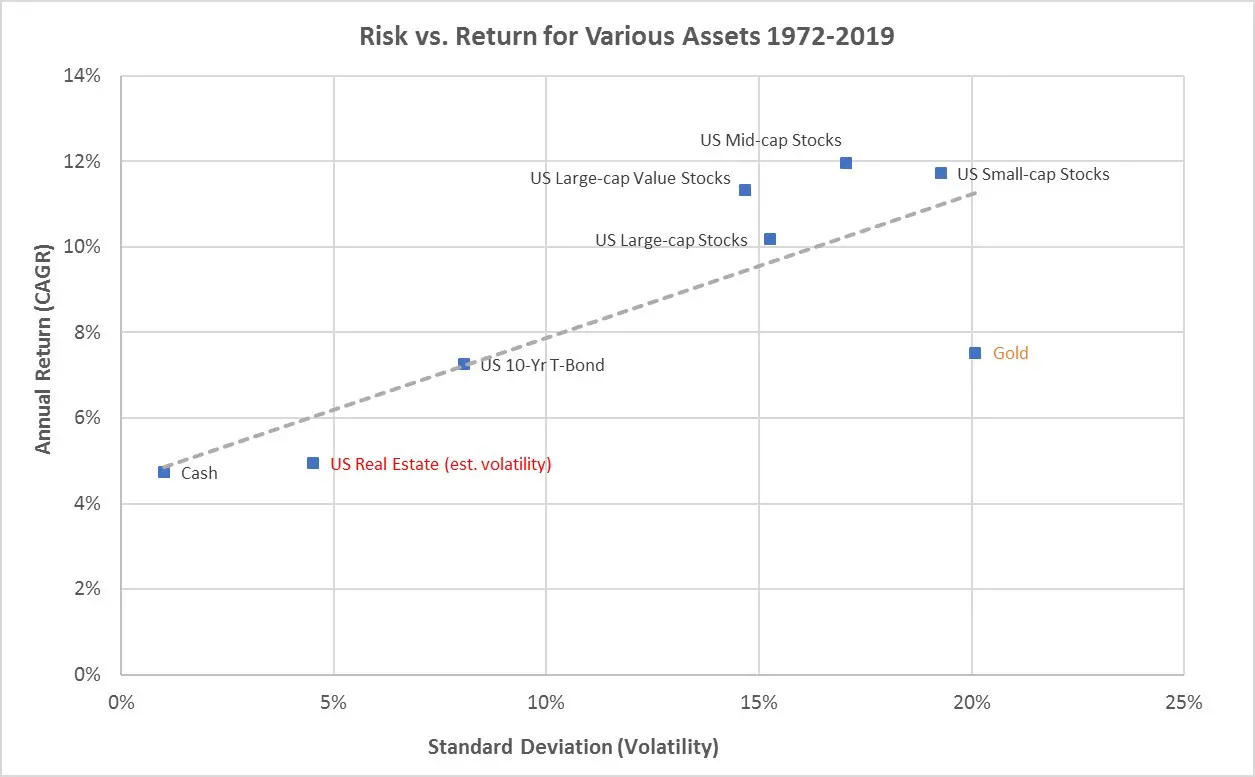

The S&P 500’s historic annual return is about 10% in comparison with solely a 4.6% historic annual return on actual property. Due to this fact, likelihood is excessive in case you promote the S&P 500 index to purchase a house with all money, your transferred capital will underperform over the long term.

The higher the share of your internet value is in a house in comparison with shares, the slower your internet value could develop. After all, your internet value might additionally outperform in case you so occur to promote shares earlier than a crash and residential costs outperform shares, as they did from 2000 – 2006.

However general, paying all money for a house by promoting shares will seemingly trigger a slowdown within the tempo of your internet value development. Alternatively, if you’re wealthy sufficient to pay for a house with idle money, then you’ve gotten a greater probability of accelerating your internet value by shopping for a house with all money.

For instance, in 2023, you are in a position to earn ~5% in a cash market fund. But when actual property costs rise by 6.5% by July 2024, as Zillow predicts, then the switch of your money to a house may make you richer. This could particularly be true if rates of interest begin to decline and actual property costs begin to speed up upward.

3) Paying all money reduces your potential returns on your property

Leverage is nice on the best way up and damaging on the best way down. When you pay all money for a house and costs go up by 5% in a single 12 months, you earn a 5% gross return. Nonetheless, in case you solely put down 20%, then your gross return in your money will increase by 25%.

The primary technique to develop your internet value quicker with actual property in contrast with shares is with a mortgage. Regardless that actual property is often thought of much less dangerous than shares, you possibly can paradoxically make much more. However that is an article about paying all money for a house.

Maybe one technique is to pay all money for a house, assess the true property market over the following 12 months or two, after which do a cash-out refinance if you’re bullish. This manner, you purchase your self extra time to make a probably extra optimum money utilization choice.

Simply remember that when it is time to entry your property’s fairness, some banks could now not provide Residence Fairness Traces of Credit score (HELOC) or cash-out refinances. Finest to double verify along with your financial institution now.

4) You lose an incredible quantity of risk-free revenue and safety

You’d assume paying all money in your residence would offer you a higher quantity of safety. As soon as you have obtained your property totally paid off, life is way simpler.

Nonetheless, here is the irony in a excessive rate of interest surroundings. When you will pay all money for a home, it means you even have the flexibility to earn a hefty quantity of risk-free revenue. This additionally means you possibly can be forgoing monetary safety.

To illustrate you possibly can pay $2 million money for a home. When you had been to simply make investments the $2 million in a 5%-yielding cash market fund, you’d earn $100,000 a 12 months risk-free. The overwhelming majority of us with no main well being points and no debt ought to be capable of fortunately reside off $100,000 a 12 months in gross revenue. Some may even think about this a Fats FIRE life-style in lower-cost areas of the nation.

However in case you determine to make the most of your $2 million money to purchase a house, your $100,000 in risk-free revenue goes away. Not solely that, however with a brand new residence, you’ll now must pay extra property taxes, insurance coverage, HOA (the place related), and ongoing upkeep bills perpetually.

Therefore, even in case you plan to purchase a house with all money, I like to recommend following my internet value information for residence shopping for. See the best three columns of the chart under. I’ll tailor the rule of thumb sooner or later for money patrons in a brand new publish.

5) You’ll nonetheless really feel anxious regardless of paying all money for a house

You’d assume paying all money for a house would provide you with super peace of thoughts. In spite of everything, with no mortgage, there is no such thing as a financial institution on the market than can take your property away from you. Even the federal government may have a tricky time kicking you out in case you do not pay your property taxes. In the meantime, a downturn in the true property market will not wipe away 100% of your fairness.

Paying all money for a house is solely an asset switch. The switch could be out of your idle money or from different investments like municipal bonds, shares, and non-public actual property investments. That stated, you’ll nonetheless really feel unsettled in regards to the asset switch as a result of the money you inject into a brand new residence turns into unproductive.

You’ll continuously wonder if there have been higher makes use of in your money than tying it up in a house chances are you’ll not want. The one technique to quiet these doubts is by creating fantastic experiences within the new residence for a number of years. However that takes time.

Your anxiousness could make you extra irritable or harassed. And a bitter temper shouldn’t be good for your loved ones and mates.

Therefore, if you will pay all money for a house, you had higher have much more money and liquid securities behind. Over time, the anxiousness ought to fade as you rebuild your money or liquid reserves.

6) It’s a must to work out what to do along with your outdated residence

When you’re presently renting and pay all money for a brand new residence, then you haven’t any worries. Give your landlord a 30-day discover or longer that you simply’re shifting out, and also you’re good to go. Simply ensure your new residence is definitely prepared to maneuver in as soon as your lease is over.

However in case you personal your current residence and purchase a brand new residence with all money, then you have to work out what to do along with your current residence. Will you rent an actual property agent to promote it? Or will you attempt to discover renters and construct your passive revenue portfolio for monetary freedom?

Personally, I like shopping for a property each 3-10 years after which renting it out when it is time to purchase one other main residence. Do that over thirty years and you’ll fund your retirement with rental properties no downside.

Feeling Nervous About Shopping for A Residence With All Money

I am contemplating shopping for one other residence with all money. However now that I am in contract with contingencies, I am second-guessing my choice, as I at all times do.

Possibly I did not must promote as many property and pay all money within the first place. Given how lengthy the escrow interval has been, taking out a mortgage would have been simply positive. However that is type of like saying perhaps I did not must have good grades and check scores after I obtained accepted to an ideal faculty!

There is a consolation in seeing different folks purchase properties throughout a bull market. It implies that different folks need what you need and are serving to justify your choice, even when it could be the fallacious one. However throughout a bear market, you’re feeling like a lonely fish out of water, questioning whether or not the tide will ever return.

Can folks merely not afford to pay all money or take out a mortgage at these charges? Or are folks ready as a result of they anticipate actual property costs to crash? It is a disconcerting feeling not understanding what’s holding folks from making the most of offers.

Why I Provided All Money

I wished to make my provide engaging sufficient for the vendor to simply accept. I used to be providing to pay 14% under final 12 months’s asking value and seven.5% under this 12 months’s new asking value. By providing to pay all money, I hoped to make my provide engaging sufficient for him to think about. Insulting a vendor with a low-ball provide shouldn’t be the best way to win offers.

Initially, the vendor declined my provide by way of his itemizing agent. However then a month glided by and the itemizing agent contacted me once more to say they might be taking the house off market. This was my final probability to make a aggressive provide!

I did not really feel a lot actual property FOMO given I used to be pleased with our current residence, so I simply stood agency on my provide value. However I additionally determined to spend 35 minutes writing an actual property love letter, explaining why my household could be an ideal selection.

The vendor wrote again a letter of his personal saying how a lot he appreciated my letter. I had touched upon every thing from how a lot I valued his transforming, to the significance of household, to our mutual love of tennis, and our related tradition. Possibly writing 2,200+ articles on Monetary Samurai since 2009 has some advantages in any case!

Then I used to be in a position to persuade the itemizing agent to scale back her general commissions by 2.5% in lieu of her additionally representing me via twin company. She initially refused as a result of she did not need to earn much less. However I defined to her she would not be incomes much less as a result of she would have needed to have paid the two.5% fee to a purchaser’s dealer anyway.

I used to be thus in a position to persuade her to offer me at the very least a 2.5% value low cost and simply signify me. It was that, or no transaction in any respect.

Elevating The Stakes By Shopping for One thing I Do not Want

As I discussed to my spouse in a earlier podcast episode (Apple), “No person wants nothing.” We do not want something greater than a studio residence, water, and cereal to outlive. Because of this, I typically query the purpose of shopping for something we do not really want. We’re frugal folks.

Paying all money for a brand new residence raises the monetary stakes as a result of it reduces our passive retirement revenue. Because of this, I’ll really feel extra strain to make more cash and develop our internet value additional.

The primary two years of possession will hold me in a heightened state of hysteria as a result of our funds might be most in danger. The anxiousness will not be debilitating to the purpose the place I will not be capable of sleep or operate. It’s going to simply be increased than I am used to since leaving work in 2012. I hope I will be capable of adapt.

Possibly I’ll use this anxiousness as motivation to write extra books and/or discover a well-paying job. When my son was born in 2017, my motivation to earn shot via the roof! Additional, I plan on giving up on early retirement anyway as soon as each children go to highschool full-time in 2024. So the celebrities appear to align.

In conclusion, pay attention to the downsides of paying all money for a house. Use your all-cash provide to get a lower cost after which rapidly replenish your money reserves after you shut. When you do, you will really feel a lot better about your buy.

Reader Questions And Recommendations

Have you ever paid all money for a house earlier than? If that’s the case, how did you’re feeling? What are another downsides to purchasing a house with money?

Do not have all money to purchase a home? No worries. You possibly can spend money on non-public actual property with Fundrise with as little as $10. Fundrise funds primarily invests in residential and industrial properties within the Sunbelt, the place valuations are decrease and yields are increased.

Hear and subscribe to The Monetary Samurai podcast on Apple or Spotify. I interview consultants of their respective fields and talk about among the most attention-grabbing matters on this website. Please share, charge, and overview!

For extra nuanced private finance content material, be part of 60,000+ others and join the free Monetary Samurai e-newsletter and posts by way of e-mail. Monetary Samurai is among the largest independently-owned private finance websites that began in 2009.