{kind=link}

Currently, there’s been a variety of speak about an absence of affordability, even a possible housing bubble.

And it comes as no shock, given the huge shock of a near-tripling of mortgage charges over only a 12 months and a half.

The 30-year fastened may very well be had within the low 3s, perhaps even excessive 2s again in early 2022, and immediately is nearer to 7%.

On the similar time, house costs haven’t come down, regardless of a slowing fee of appreciation.

Collectively, this has introduced the housing market to its knees and pushed many potential patrons onto the sidelines. However those that promote are nonetheless reaping large earnings.

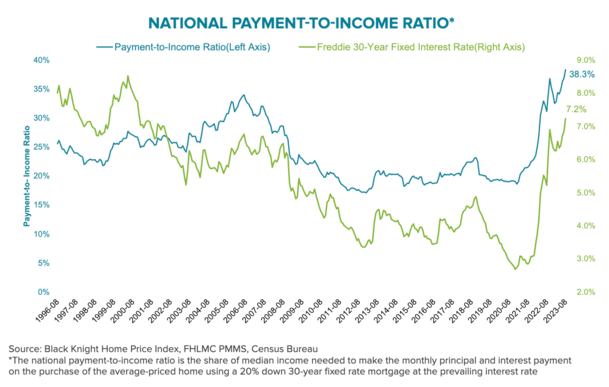

Residence Shopping for Is the Least Inexpensive Since 1984

Bear in mind these Eighties mortgage charges that had been within the double-digits? Nicely, immediately’s mortgage charges are nowhere shut.

Nevertheless, as a result of sky-high house costs and elevated rates of interest, house shopping for is the least inexpensive it has been since 1984.

That’s proper, it hasn’t been this dangerous in about 40 years, which illustrates simply how difficult this housing market has grow to be.

Per Black Knight, it now requires 38.3% of the median family revenue to make a month-to-month mortgage fee on an average-priced house.

Utilizing Freddie Mac’s 7.23% common for a conforming 30-year fastened mortgage as of August twenty fourth, the month-to-month principal and curiosity fee climbed to $2,423.

And this assumes the customer is available in with a 20% down fee, when in actuality many debtors can solely muster 3-5%.

To the purpose of it being a bubble, it might take some heavy lifting to carry affordability again to its 25-year common.

We’re speaking some mixture of a ~27% decline in house costs, a 4%+ discount in 30-year mortgage charges, or a whopping 60% improve in median family.

Which of these three do you suppose are likeliest to transpire? In all probability none of them barring one other large housing crash.

However a mixture of the primary two is affordable, whether or not it’s a ten% drop in house costs and a 2% drop in mortgage charges. Or another mixture.

It’s unclear if wages are going to see a lot enchancment from right here on out, definitely nowhere near 60%.

For perspective, the 30-year fastened averaged about 13.2% the final time housing affordability was this dangerous.

This tells you house worth progress has far outpaced wage progress, primarily demanding low rates of interest bridge the hole.

Regardless of this, house sellers are racking up large good points, due to double-digit house worth appreciation over the previous a number of years.

The Few Residence Sellers Out There Are Raking in Massive Earnings

Redfin reported immediately that 97% of house sellers bought for a revenue throughout the three months ending July thirty first.

And the standard property that bought went for a whopping 78.4% greater than the vendor paid, or $203,232.

Whereas there’s a extreme lack of affordability in immediately’s housing market, there appears to be a good greater scarcity of houses to buy.

As such, house costs stay on the up and up, permitting the few sellers on the market to absorb a tidy revenue.

The vast majority of sellers bought their houses properly earlier than property values skyrocketed, making it fairly simple to snag a six-figure acquire.

San Jose leads the nation in median capital acquire at a staggering $755,000. It’s additionally 108.6% greater than what the vendor paid.

San Francisco isn’t far behind at $625,500 and 70.5%, respectively, adopted by Anaheim at $470,000 and 88.7%.

Even Detroit, which ranked final when it comes to greenback good points of the 50 metros analyzed noticed a median $80,500 capital acquire.

If we think about proportion good points, Fort Lauderdale topped the checklist with a 122.2% cap acquire, adopted by San Jose and Miami.

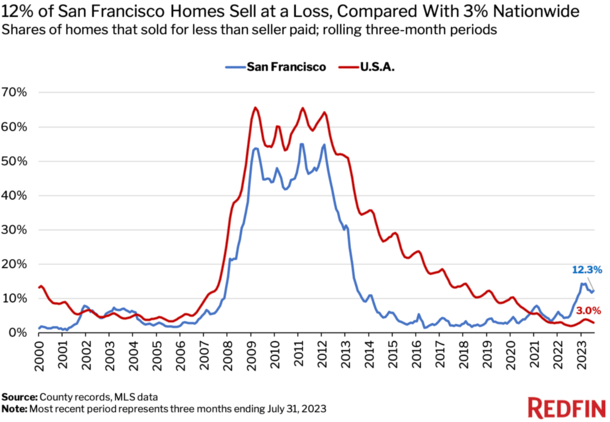

Some Residence Sellers Are Shedding Cash, Particularly in San Francisco

Whereas most sellers are making out like bandits, Redfin did observe that some house sellers are parting with their properties at a loss.

That is very true in San Francisco, which has struggled with falling property values and tech layoffs.

San Francisco’s median house sale worth fell a file 13.3% year-over-year from April 2022 to April 2023, greater than triple the nationwide decline of 4.2% at the moment.

However as of July, costs had been down simply 4.3% year-over-year, considerably nearer to the nationwide acquire of 1.6%.

This would possibly clarify why 12% of house sellers in San Francisco bought for a loss throughout the three months ending July thirty first.

Put one other method, one in every of each eight houses that bought throughout this era went for lower than what the vendor paid.

And the standard vendor bought for about $100,000 lower than what they paid, tying New York for the most important median loss in {dollars}.

Nationwide, the standard home-owner who bought for a loss solely bought for $35,538 lower than what they paid.

Different main metros that had a excessive proportion of sellers taking a loss included Detroit (6.9%), Chicago (6.5%), New York (5.9%), and Cleveland (5.8%).

One Redfin Premier agent mentioned some condos within the Bay Space are promoting beneath 2018/2019 buy costs as a result of commuting into downtown San Francisco is now not “a factor anymore.”

In the meantime, an agent in Boise mentioned some purchasers might want to promote at a $100,000 loss as they transfer again to Seattle as a result of work-from-home (WFH) has ended they usually purchased the properties lately.

However the worth level on such transactions is mostly above $750,000, which most likely isn’t your typical house in that a part of Idaho.

And as you’ll be able to see from the chart above, only a few houses are promoting for beneath what the vendor initially paid.

So earlier than we get enthusiastic about one other brief sale wave, as seen within the early 2000s, we might wish to mood our expectations.

After all, market situations can change quick. For instance, a 12 months in the past solely 0.2% of Austin houses bought at a loss versus 3% in the identical interval this 12 months.

Austin had the bottom share of house gross sales at a lack of the highest 50 metros. Not so anymore.