{kind=link}

A reader asks:

To not brag (simply kidding), however I’m 38, make $50k/yr and have $10k in Marcus, $10k in an Roth IRA, $10k Crypto, and $10k Conventional 401k. My web value is about $50k. My bills are about $40k per yr and I can sometimes save about $500 per 30 days. I stay in Los Angeles with my companion. For low incomes people who wish to be financially steady what recommendation do you will have? My POV is that I’ve such a small amount of cash and I’m 38 so it doesn’t actually matter as a result of the period of time to compound is shorter and my accessible month-to-month funding is low. For decrease revenue people/listeners, ought to I simply spend it as a result of the reward of compounding takes so lengthy. I really feel time is just not on my aspect. I’m not aggressive within the labor market (I graduated from Arizona State College lol). Getting an MBA isn’t within the deck of playing cards. I work as a resident providers coordinator for an inexpensive housing group in Santa Monica. I’ve my 6 months of financial savings locked in and don’t contact it.

You’re promoting your self quick right here.

The truth that you’ll be able to afford to stay in California and nonetheless save $500 a month in your wage is spectacular. You’ve a six-month emergency fund. Plus you will have a web value that matches your revenue.

And also you’re not even 40!

You say you don’t have sufficient time to permit compounding to work however I don’t suppose that’s true. Individuals usually underestimate the facility of compounding over a number of a long time as a result of the outcomes take time to play out.

You continue to have loads of time.

Let’s take a look at a couple of examples to see how issues are arrange for you presently and the way you would enhance your scenario.

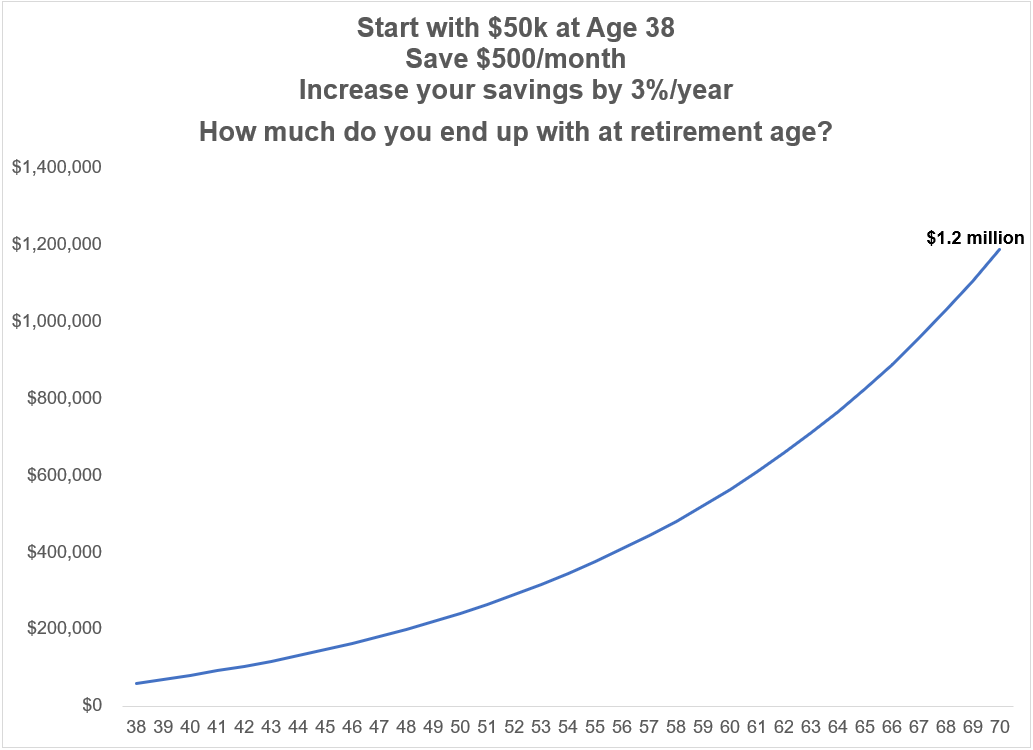

Proper now you will have $50,000 saved and put away $6,000 a yr. Assuming you develop that $50k beginning worth at 6% per yr and enhance your financial savings fee by 3% every year1 to account for inflation, right here’s how issues would look going out to age 70:

By age 65 you’ll have greater than $822,000. In case you waited to retire till age 70 we’re speaking nearer to $1.2 million.

Not unhealthy, proper?

There are lots of assumptions baked into this evaluation however in case you keep on the identical monitor you’re on and permit compounding to do the heavy lifting for you, that’s a reasonably good consequence.

I feel we are able to do higher than this.

First, let’s see how far some extra frugality or some form of aspect hustle might take you.

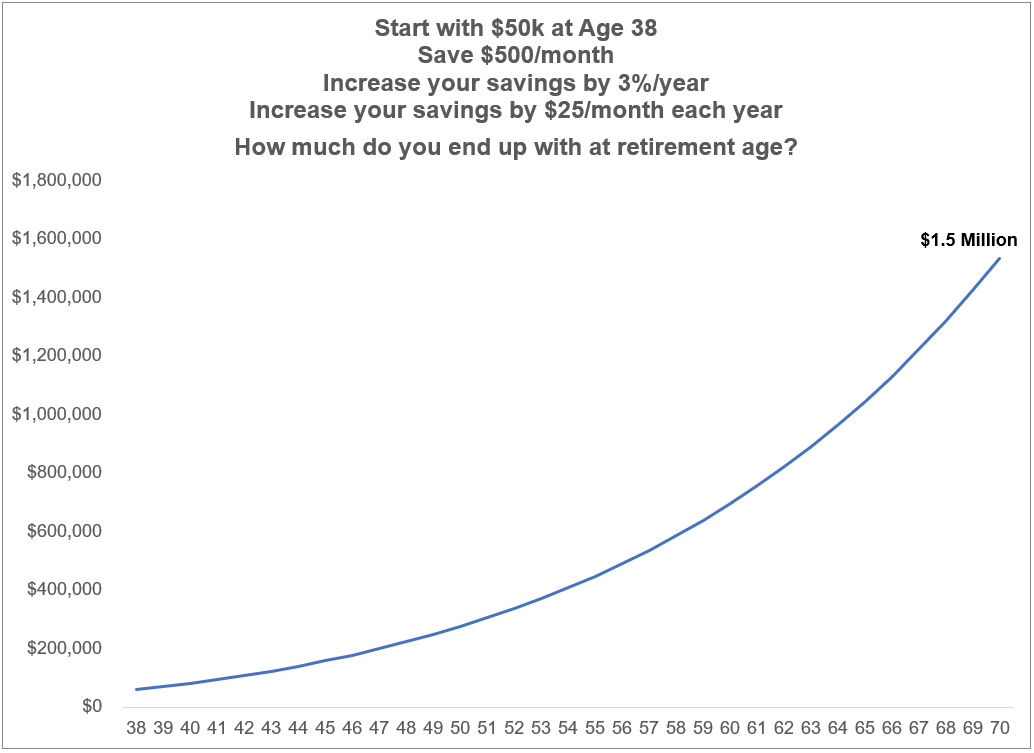

Let’s say you save an additional $25/month every year on prime of those assumptions. That’s simply $300 extra in financial savings every year on prime of what you’re already saving. Now we’re taking a look at slightly greater than $1 million by age 65 or $1.5 million by age 70:

Small adjustments can have a big impact over multi-decade time horizons.

Nevertheless, frugality can solely get you up to now, particularly on a decrease revenue.

The soiled secret of private finance is revenue is by far the most important lever you’ll be able to pull to enhance your funds.

Possibly you’re pleased with the job you will have and don’t care about your revenue degree.

However now’s the proper time to no less than discover your choices.

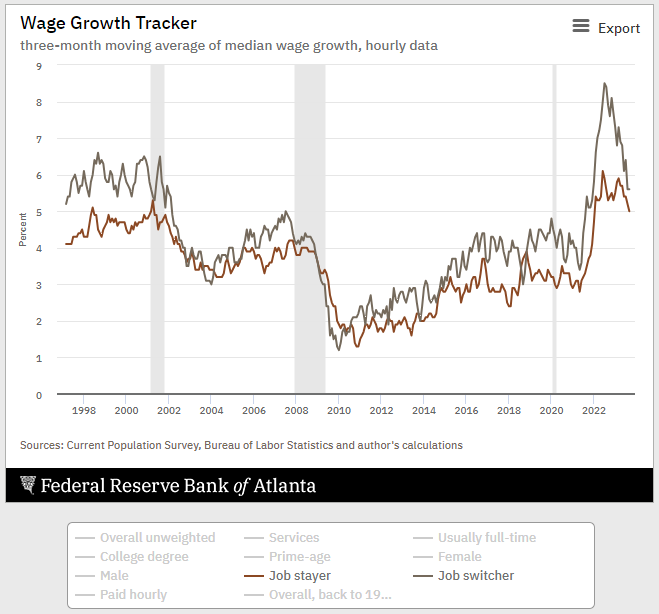

Simply take a look at the Fed information on wage progress numbers damaged out by job switchers and job stayers:

Because the begin of 2022, individuals who have switched jobs are averaging almost 7% annual wage progress versus 5% annualized wage progress for job stayers.

In case you ever needed to check the waters now’s the time to take action.

A single elevate early in your profession can have a large affect in your funds.

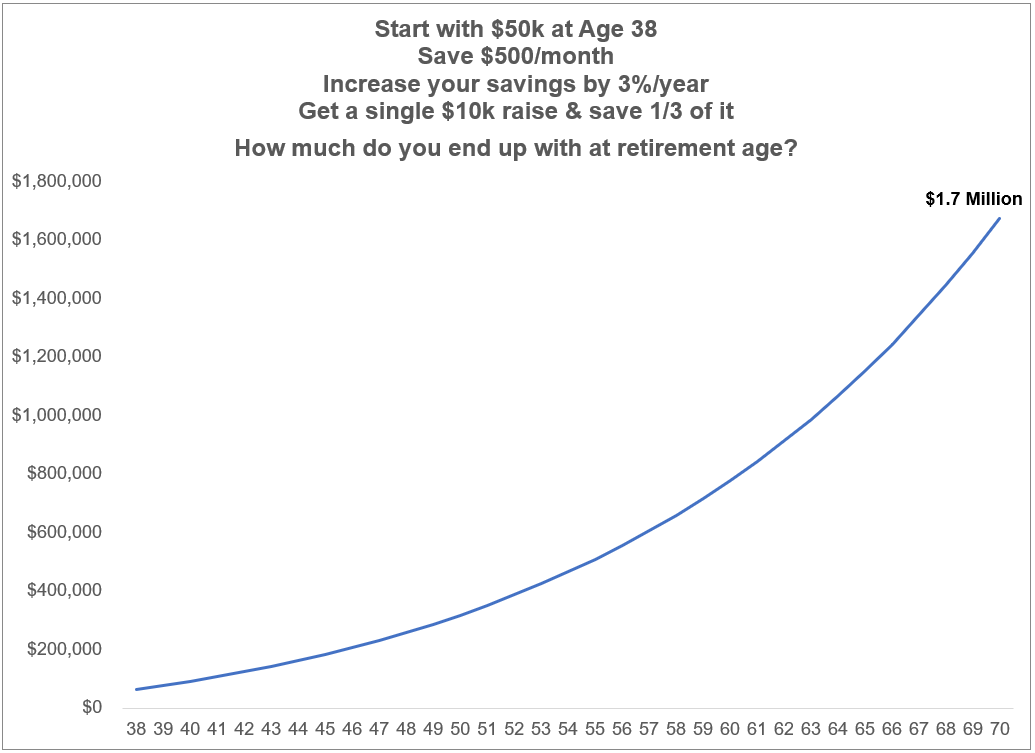

Let’s say discover a new job that pays you $10,000 greater than you’re presently incomes. It won’t be your dream job however we’re nonetheless in a decent labor market. Let’s additionally assume you save roughly 1/3 of that elevate yearly ($3,500). So we go from $6,000/yr in financial savings in yr one to $9,500/yr (and enhance that by 3% every year for inflation).

That pushes your ending worth at age 65 to $1.1 million or $1.7 million in case you preserve saving till age 70:

Once more, not unhealthy.

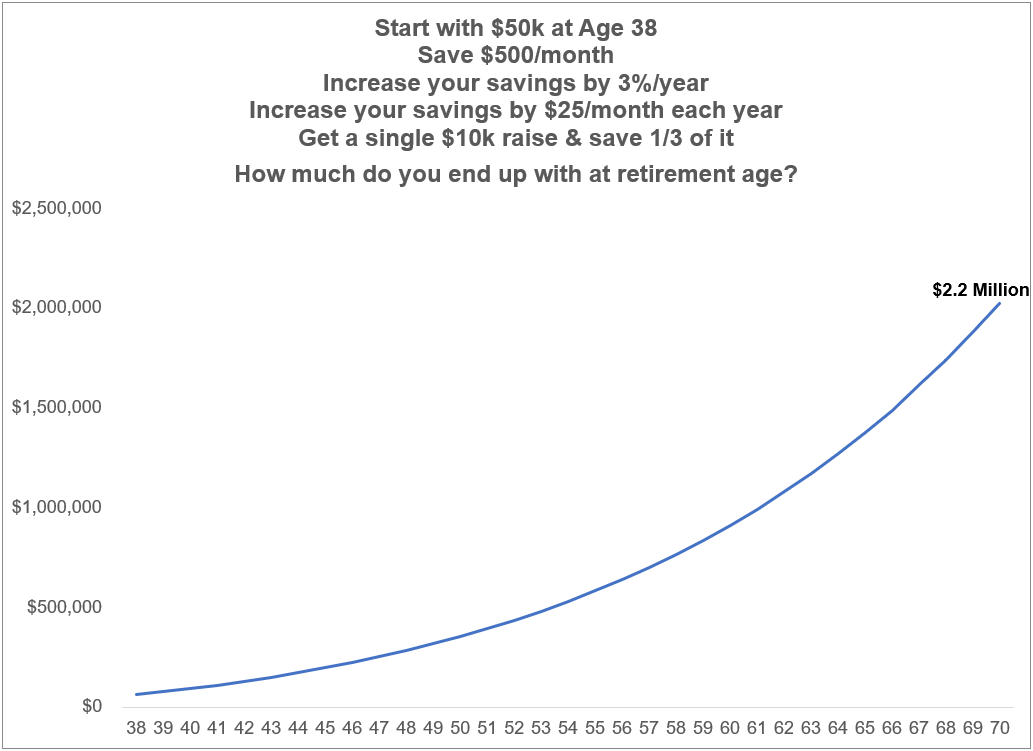

Now, what if we mix the 2 methods?

First you discover a new job or negotiate the next wage and bump up your financial savings by simply $25/month every year.

Now we’re speaking:

That’s simply shy of $1.4 million by age 65 and $2.2 million by age 70.

One $10k elevate and $25/month in additional financial savings may very well be value $1 million over a three-decade-plus time horizon.

Clearly, life by no means works out like a spreadsheet. Some years you’ll be capable to save extra. Some much less.

Your profession trajectory may match out higher than you anticipate. Or worse.

Your funding returns may are available greater. Possibly decrease.

The primary takeaway right here is the way in which to save lots of on a decrease revenue is similar method you must save at the next revenue:

- Stay on lower than you earn

- Automate your financial savings

- Enhance your financial savings fee every year

- Save slightly more cash every year

- Enhance your incomes potential

The excellent news is you already know easy methods to save. Stick with it and you’ll nonetheless construct a pleasant nest egg.

However there are additionally methods to enhance your scenario in case you’re keen to work in your profession and save slightly more cash every year.

We mentioned this query on the most recent version of Ask the Compound:

Kevin Younger joined me once more this week to debate questions starting from anticipated returns in company bonds, the most effective month to take a position a lump sum, organising an account to pay to your youngster’s healthcare prices, the place pensions match right into a monetary plan and easy methods to allocate property from life insurance coverage.

Additional Studying:

Earnings Alpha

13% per yr may sound like rather a lot however that’s a rise of $180 the primary yr (not per 30 days, for the entire yr), $185 the second yr and $191 in yr three. It’s doable particularly since your revenue also needs to preserve tempo with inflation.